In January, May and October the monthly letter is replaced by a Focus Trimestriel that identifies one or more themes currently on my radar. It is somewhat longer; there are charts. I rely on your patience.

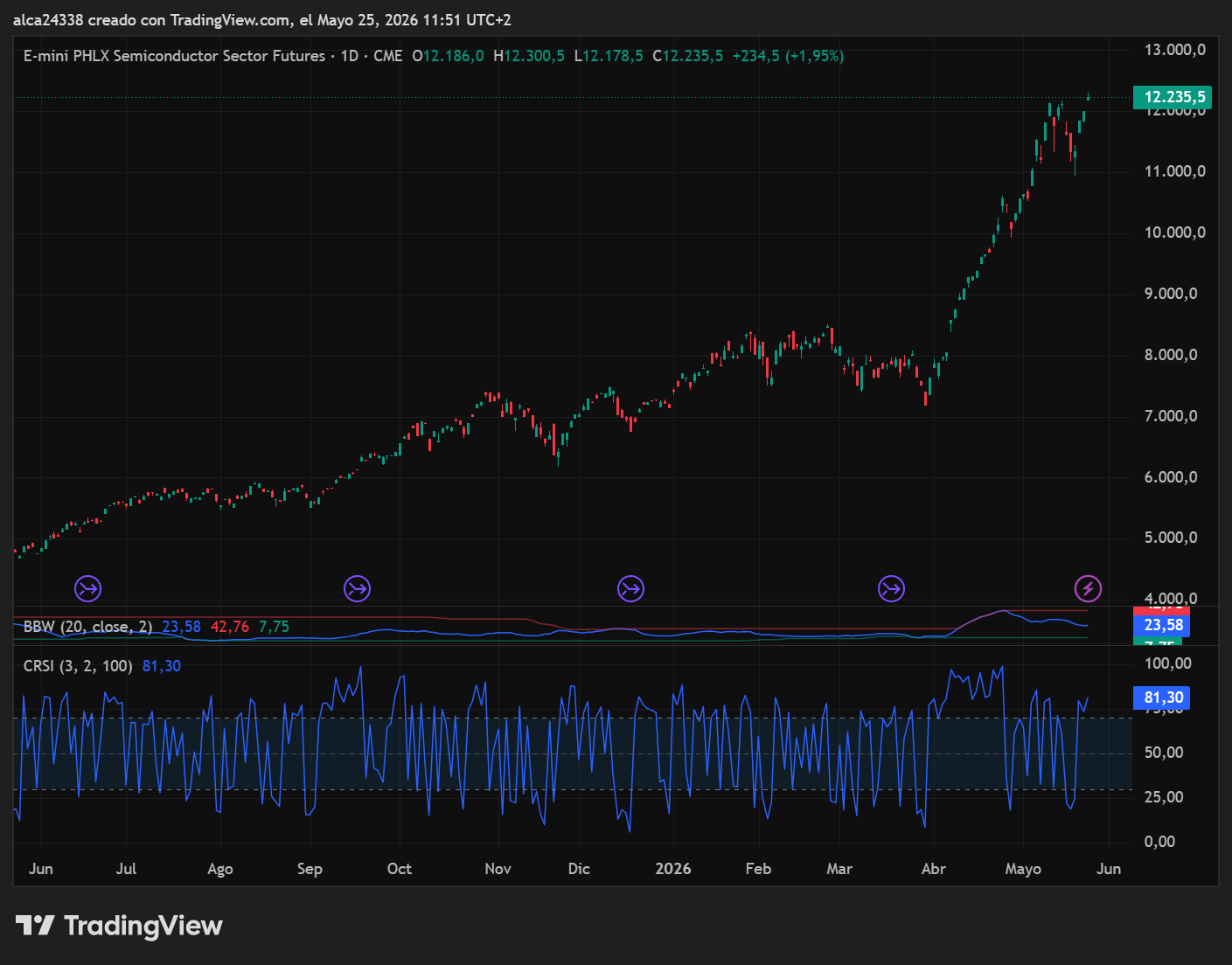

Le rally des actions amorcé depuis les creux de fin avril 2025 a été porté par le thème de l'IA — et des semi-conducteurs en particulier.

Le SOX (indice des semi-conducteurs de Philadelphie) a triplé de valeur en un an.

L'indice national le plus aligné sur le SOX est le coréen KOSPI200. Lui aussi a triplé de valeur en un an.

Les trois principales compagnies d'assurance sud-coréennes ont déclaré qu'environ 16 % des assurés ont liquidé leurs fonds de pension pour investir en bourse au premier trimestre 2026.

Un chiffre énorme.

Normalement, les rachats de fonds de pension ne dépassaient pas 3 % par an.

Ces comportements sont cycliques et se répètent dans toutes les phases exponentielles et finales d'une bulle.

Les moins jeunes se souviendront de l'an 2000 : des gens ordinaires vendant maisons et entreprises pour participer à la folie des Dotcom.

Débloquons un souvenir : entre 1999 et 2000, le mantra de la Silicon Valley était « Get big fast » — sacrifier les profits sur l'autel de la notoriété de la marque.

En janvier 2000, Pets.com acheta un espace publicitaire de 30 secondes pendant le Super Bowl XXXIV, dépensant plus de deux millions de dollars pour lancer sa mascotte — un chien-marionnette en chaussette.

Le spot fut un succès culturel extraordinaire : la mascotte apparut même dans le défilé de Macy's.

Pourtant, entre février et septembre 1999, la société avait déjà dépensé 70 millions de dollars en marketing pour seulement 619 000 dollars de revenus.

Pendant ce temps, dans un garage de Seattle, un jeune Jeff Bezos se creusait la tête pour vendre des livres en ligne, essayant de dépenser moins que ce qu'il (peu) gagnait.

En mars 2000, la bulle dot-com éclata. En novembre de cette même année, neuf mois après le Super Bowl, Pets.com déposa le bilan et disparut.

Amazon est toujours là. Depuis ce novembre 2000, elle a multiplié sa valeur par 270 — quiconque aurait investi 10 000 dollars le 30 novembre 2000 aurait aujourd'hui 2 700 000 dollars.

Since I have been in markets, at least a couple of times a year someone appears predicting a new 1929.

They may not even believe it themselves.

Prophets of doom sell better than those who limit themselves to an analysis of the facts.

Prédire des catastrophes fait de l'audience ; essayer d'écouter le souffle du marché, beaucoup moins.

And many predict an apocalypse when the AI bubble bursts.

As in every technological leap, the challenges are real.

OpenAI a une situation d'endettement difficilement soutenable à moyen terme.

Or rather: OpenAI finds itself in a paradoxical financial position.

La société est presque exempte de dette directe à long terme, mais a accumulé des engagements de dépenses en infrastructure et cloud de plus de 1 400 milliards de dollars pour les prochaines années.

To finance its enormous computing needs without taking on debt directly, Altman's company has shifted the risk onto logistics partners — SoftBank, Oracle and CoreWeave — which have taken on around $100 billion in debt to build the data centres dedicated to it.

Malgré des revenus autour de 20 milliards de dollars, OpenAI brûle constamment de la trésorerie et prévoit des pertes de 14 milliards.

For this reason it relies continuously on massive private investment rounds to avoid running out of liquidity.

C'est le cas classique de qui essaie de devenir quelque chose de trop grand pour faire faillite.

Sometimes it works — we have discussed Tether many times, and its vast murky areas concealed by its even larger capitalisation.

Sometimes it does not. And then things get painful.

L'introduction en bourse d'OpenAI est annoncée pour septembre. Il sera intéressant de suivre.

On the other side, there are companies like Anthropic which — regardless of ethical and political considerations that are not relevant here — have all the characteristics needed to survive any crisis and perhaps even to lead the next one.

There is also an ecosystem developing.

Copper miners, nuclear energy.

Old favourites of mine like Plug Power, which seem to signal a returning interest in hydrogen.

Le point névralgique est clair : tel quel, l'IA consomme une quantité de ressources — énergétiques surtout, mais pas seulement — insoutenable à moyen terme.

The challenge is to find ways of limiting its energy impact.

Various projects are developing in this direction: I am thinking of Kairos Power and the agreement between Microsoft and Constellation.

I am also thinking of neuromorphic chips, capable of reducing consumption peaks by more than 80% compared to a standard GPU.

This is where the real contest will be played out, in my view.

La bulle de l'IA va éclater, comme toutes les autres, parce que c'est ce que font les bulles : elles éclatent.

But bubbles do not always cancel an entire sector when they burst.

Sometimes the burst is merely a rebalancing of excesses and a redistribution of power — a return to the mean, as those who speak well like to say (not my case).

Exactly what happened with the Dot-coms.

And what will happen with AI.

Qui est là pour rester : mieux vaut s'y faire.

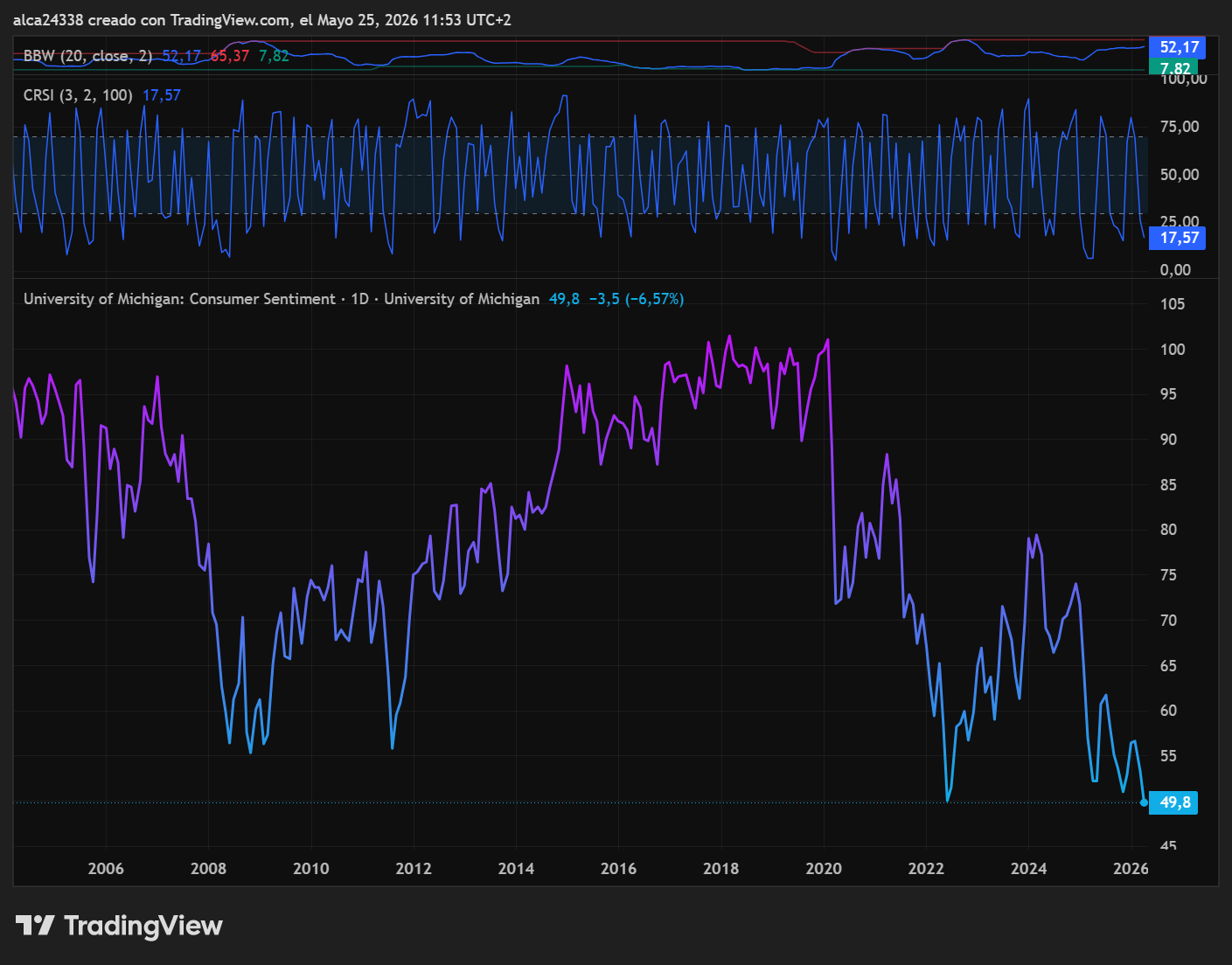

L'indice de confiance des consommateurs de l'Université du Michigan a enregistré un plancher historique absolu dans sa dernière lecture préliminaire de mai, à 48,2 points.

This figure must be read against the backdrop of the all-time equity highs discussed above.

The 48.2 reading in May represents the lowest level ever recorded since the University of Michigan's series began in 1952.

The current reading is even below the historical lows reached during the 2008 financial crisis — whose negative peak was 55.3 in November 2008 — and is also below the levels seen during the inflationary shocks of the early 1980s and the Covid-19 lockdowns.

Classical economic theory holds that low consumer confidence leads to recession and equity falls.

It is a topos found in every basic economics textbook.

There is a logic to it: if the consumer is depressed and stops spending, the economy stagnates and with it the market.

I have no intention of arguing against this.

I would, however, venture an alternative view that I hope will not seem excessively conceptual.

If equity markets are at all-time highs, reflationary pressures are significantly on the rise, and bonds are falling — all while consumer confidence sits at 74-year lows — what would happen if confidence returned toward its historical average?

Belle confrontation : confiance des consommateurs contre tendance du marché.

Été du Cycle K. Reflation.

Comme je l'ai dit à maintes reprises dans les lettres précédentes, en octobre 2022, je crois que la transition du Printemps à l'Été du cycle de Kondratiev a commencé. Until the markets signal that I have taken a wrong course, this will be my map.

For those interested in exploring what I describe below, I recommend the wonderful book Inventing Money by N. Dunbar, published in 1999 by Wiley, which tells the story of the birth, triumph and shipwreck of Long-Term Capital Management.

In 1994, Long-Term Capital Management was founded by John Meriwether alongside Nobel laureates Robert Merton and Myron Scholes.

The fund achieved extraordinary returns through bond arbitrage and derivatives with enormous leverage.

The strategy rested on the assumption that spreads between similar instruments would revert to normal.

After the Russian default of October 1998, correlations broke down, spreads exploded and LTCM lost nearly all its capital within weeks.

The fund was aimed at large financial institutions and government entities.

Its failure triggered a violent but short-lived systemic crisis.

After falling more than 30% in a few weeks, the S&P 500 quickly recovered all lost ground, closed the year at highs and laid the foundations for the exponential 1999 rally that carried markets to the absolute peaks of March 2000.

1998 was the fourth and final year of the US Presidential Cycle — running from the last full year of the outgoing president to the subsequent mid-term elections — and also the seventh and final year of the Composite Septennial Cycle.

An intersection that occurs every 28 years.

Add 28 to 1998…

In years when these two cycles intersect, events of geopolitical or financial significance tend to occur, with important market implications:

1858: following the collapse in grain prices and the failure of four of the major American railway companies between 1857 and 1858, a wave of bank insolvencies swept North America and England, crippling entire regions of both countries.

1886: the year of the second American industrial revolution, a US stock market boom. The world's largest gold deposit was discovered in the Northern Transvaal; the enormous quantity of gold released onto the market definitively consolidated the Gold Standard.

1914: outbreak of the Great War, global financial panic, the secular low of the Dow Jones that laid the foundations for the great 1915 rebound.

1942: the effective entry of the USA into the Second World War, beginning of the great War's Bull Market.

1970: culmination of racial tensions across the USA, beginning of the dismantling of the Bretton Woods system.

We have already discussed 1998.

I am confident you have done the arithmetic correctly. You will find that 2026 is the year of the intersection between the end of the Presidential Cycle and the Composite Septennial.

A characteristic common to all the years considered above is that each carried within it a more or less violent stress event, followed by a rally in equity markets in the subsequent year or two.

Between May 26 and November 9, there are three cluster points on the weekly cycles that could lead to a significant equity correction.

Statistics, of course. Not certainty.

The geopolitical issues on the table are many. The potential systemic triggers too.

When Russia invaded Ukraine in February 2022, Kyiv's industrial capacity for building attack drones was infinitesimal.

In 2023 the first Ukrainian drone strikes began — few, short-range, more demonstrative than strategic. By 2024 the strikes had become medium-range, targeting strategic installations in Russia's energy supply chain.

In October of that year, Putin updated Russia's nuclear protocol, declaring that Moscow would be justified in using tactical nuclear weapons in the event of attacks on the Russian population.

On Sunday May 17, a highly detailed WSJ article described a series of Ukrainian strikes on the urban area of the Russian capital, reportedly causing three deaths, dozens of injuries and damage to various infrastructure.

The same article discussed the exponential growth of Kyiv's industrial capacity — which now not only commands large drone numbers for its own use but is also exporting them to the Gulf region.

Discontent is growing in Russia, and strikes at the heart of the capital could back Putin into a corner.

Ne coincez jamais un rat.

The only hope comes from the RTS Index. The Moscow index is flirting with the 1,200 area, which has repelled every upside breakout attempt since 2022. This time it appears to approach it with more momentum.

An upside breakout could signal a possible turning point in the conflict.

Aucun des deux belligérants n'admettra jamais une défaite.

Mais un gel du statu quo et une trêve sine die pourraient donner aux deux parties la possibilité de présenter l'issue en interne comme une victoire et ramener l'oligarque à de plus modestes intentions.

Trump s'est embourbé en Iran. Israël n'acceptera pas facilement un désengagement américain qui ne soit que façade. Les élections de mid-term approchent à grands pas et la popularité du duo dynamique à la tête de la Maison Blanche est en chute libre. Des sources proches de l'administration ont rapporté le 17 mai que Cuba aurait acheté « more than 300 military drones » et discuterait de leur utilisation contre Guantanamo.

Évidemment, personne n'y croit.

Peu importe.

L'annexion de Cuba, formelle ou non, comme 51e État pourrait bien revenir à la mode avant le 3 novembre.

Dans la nuit du lundi 18 mai, l'obligation japonaise à 30 ans a atteint le rendement le plus élevé de ce siècle, touchant les 4,2 %.

Au même instant, l'équivalent américain — le T-Note à 30 ans — rapportait 5,088 %.

Pour la première fois, le delta entre les taux japonais et américains à 30 ans est tombé sous 1 %. On average, from the mid-1990s to today, it has been above 3% and has very rarely dropped below 2%.

Les Japonais — et plus généralement les Asiatiques qui referencient historiquement le yen — sont parmi les plus grands détenteurs de la dette publique américaine.

The yen-to-USD carry trade, which made sense when the yield differential was high, now makes far less sense at below 1%.

Ce n'est pas un canari dans la mine. C'est un faisan, ou un vautour, ou tout grand oiseau qui vous vient à l'esprit.

Naturally, the central banks — the Fed, BOJ and BOE above all — are fully aware and will act to neutralise the threat.

The ECB, meanwhile, will watch from the sidelines. European long-dated bonds are now, for perhaps the first time ever, yielding below their Japanese equivalents.

Much of the ECB's decision-making power traces back to the Bundesbank, which — however bizarre it may seem at a century's remove — has as its primary mandate the prevention of a new Weimar.

Returning to non-EU central banks: they often succeed in their aims.

Sometimes, though, things get out of hand.

There is one indicator I will be watching closely in the coming months: the USD/JPY exchange rate.

For now it is quiet around 160.

En dessous de 145, le faisan dans la mine devient un vautour.

En dessous de 140, le vautour devient un ptérodactyle.

And in that case I might change my approach to equities.

As long as the yen/USD cross remains at current levels this is merely a warning and nothing more. And my strategy will not change: I will buy equities in the event of corrections in the second half of the year.

Comme toujours, l'analyse de la volatilité gouvernera le timing d'entrée.

In my previous report I anticipated a VIX remaining compressed between 15 and 25 points.

That proved to be the case, creating a favourable environment for the short strategy set up for May. Good.

For June the overall structure does not change, but I would expect volatility to increase progressively. A compact must be made with the market: rising daily premiums are matched by compressed monthly premiums.

An environment favourable to a long monthly straddle combined with two short 3-day strangles per week. Naturally, careful attention must be paid to strike selection and changes in skew.

More details in the weekly report dedicated to options trading.

Comme communiqué en temps réel, le 25 mai j'ai effectué plusieurs opérations de sortie et d'entrée.

Ventes : je suis sorti de la position longue sur le RTY, encaissant 39 % sur le trade. Je reste long uniquement sur le FTMIB, qui continue de montrer une force relative vraiment impressionnante. J'ai clôturé le spread Bitcoin vs Ethereum car il était en terra incognita ; le rendement de 3,7 % sur la position était dérisoire, mais je voulais libérer de la liquidité pour préparer les nouvelles opérations qui pourraient se présenter dans le second semestre.

Achats : le 18 mai, j'ai acheté 5 % en café à 264,50 dollars. C'est une position que j'aimerais renforcer sur faiblesse et conserver longtemps.

| Position | Poids | Ouverte | Entrée | Current | P&L % | Notes | |

|---|---|---|---|---|---|---|---|

| Long WEAT | 5% | 18.11.2025 | 549.05 | 647.38 | +18.2% | ||

| } | Long KC Coffee | 5% | 18.05.2026 | 264.50 | 272.00 | +2.8% | |

| Long FTMIB | 10% | 10.04.2025 | 34,275 | 47,890 | +39.7% | ||

| Liquidités | 80% | — | — | — | — |

Dans la première semaine de mai, j'ai eu au moins deux occasions de renforcer ma position sur le blé (WEAT) et je ne les ai pas saisies. Il y aura peut-être d'autres occasions, mais pour la clarté opérationnelle : quand l'opportunité d'entrer se présente, il faut en profiter — cela libère l'attention d'un marché et permet de se concentrer sur d'autres.

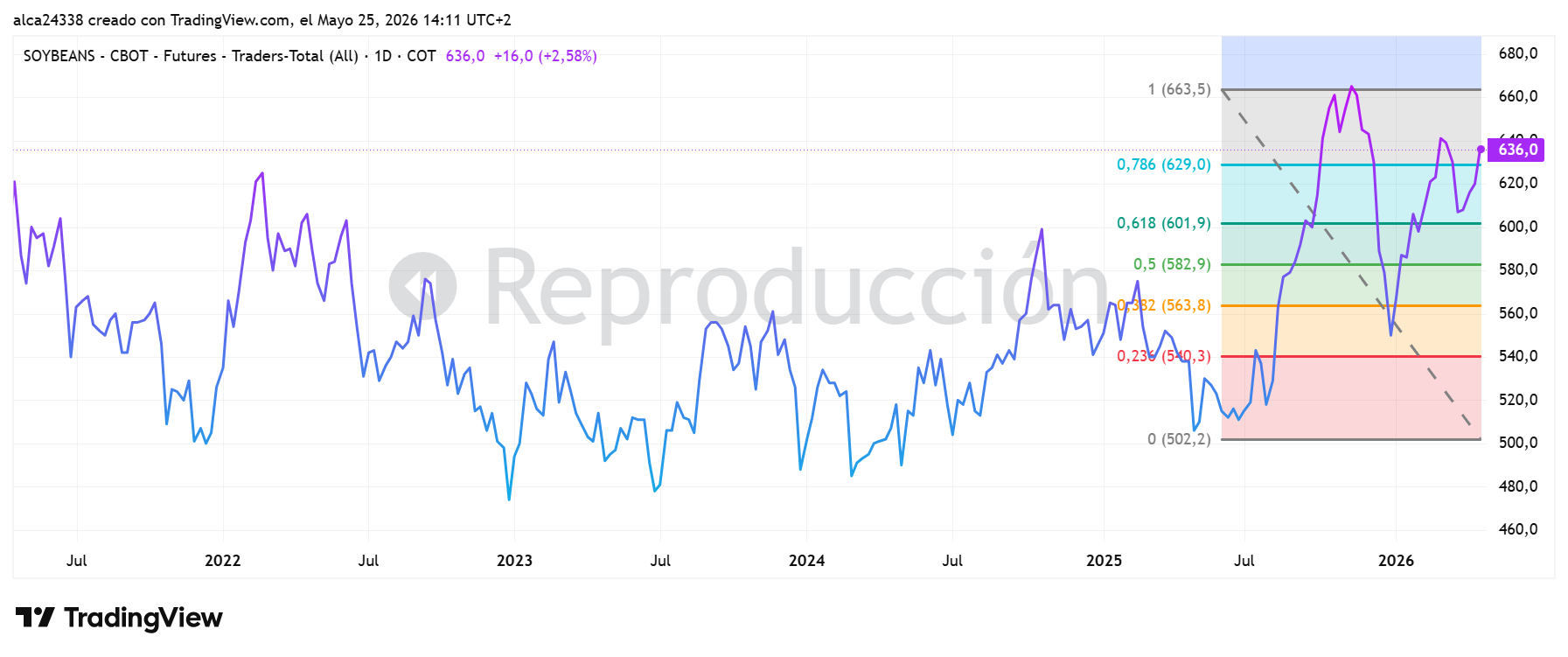

Je continue à surveiller le soja — voir la lettre de fin avril.

Le KC Coffee a un setup très contrasté. À court terme, il semble prêt à corriger, avec de la place pour une baisse de 10 à 15 %. À plus long terme, cependant, il semble se recharger.

Je mettrai à jour en temps réel, comme toujours, sur les opérations qui modifient mon portefeuille.

«Personne, c'est mon nom — Personne m'appellent père et mère» — Homère, Odyssée, IX